Why the Car Lease vs Buy Debate Is Closer Than You Think

The math changes when you account for loan balances

Money Matters

The car lease versus buy debate usually comes down to this: dealers push leasing because of lower monthly payments, while financial advisors push buying because “you build equity.” But both sides often get the math wrong.

I decided to run the real numbers on a $50,000 car purchase, and the results surprised me. Unlike the dramatic differences you’ll see in most analyses, the true cost comparison is much closer than people think…at least over short time periods.

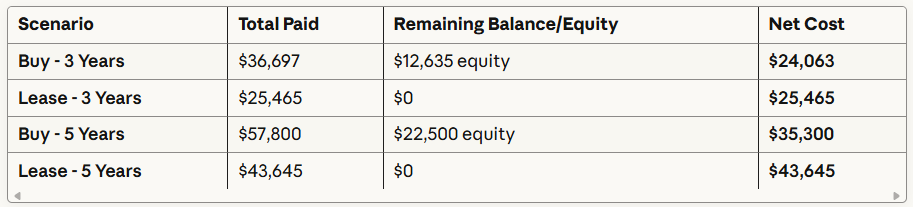

Here’s what the correct math shows:

The key insight most analyses miss: when you buy a car with financing and sell it after three years, you still owe a substantial amount on the loan. After 36 payments on a $45,000 loan at 6.5%, you still owe nearly $20,000. That remaining balance dramatically reduces your net equity compared to the gross resale value.

Over three years, buying saves you only $1,402…about 5.5% less than leasing. That’s significant, but not the massive difference most financial content claims. The real advantage of buying emerges over longer time periods, where the savings grow to $7,703 over five years.

IF a particular vehicle make/model depreciates faster than others…. or you don’t accomplish good trade-in value…. the 3-year lease option could come out ahead

The mistake most people make is focusing on monthly payments ($880 to buy versus $676 to lease) instead of understanding the total cost equation. But the bigger mistake is not accounting for loan payoff amounts when calculating equity.

Action Steps

Keep reading with a 7-day free trial

Subscribe to In Leyman's Terms to keep reading this post and get 7 days of free access to the full post archives.